July 28, 2025

mins read

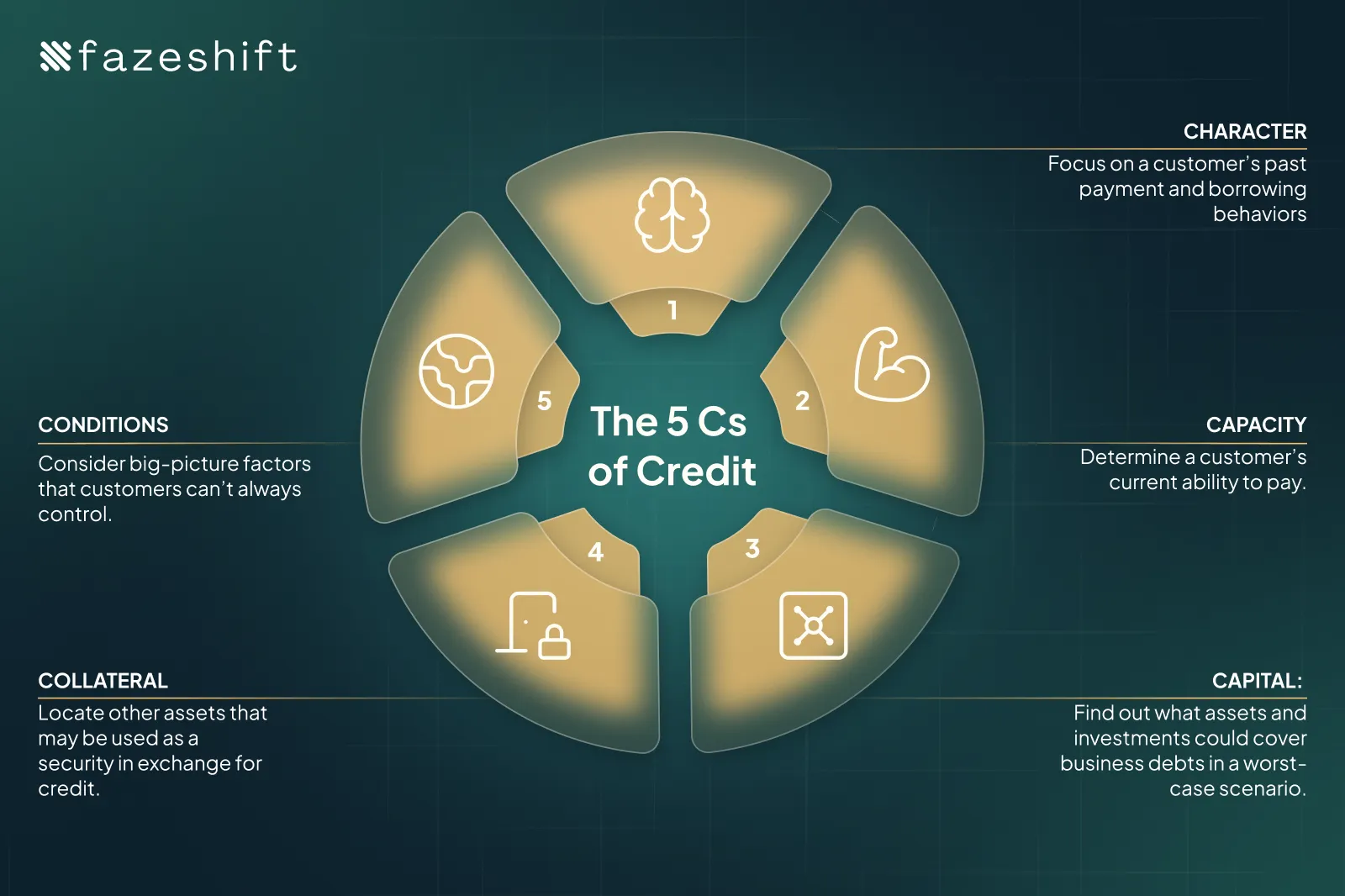

The 5 Cs in Credit Management for Accounts Receivable

Share with others

Protecting your organization from unnecessary financial risk is more important than ever.

You need to make sure that only the most predictably reliable and financially stable customers can be offered higher credit limits, favorable payment terms, and lower interest rates.

Effective credit risk assessment ensures you're working with customers who can and will pay their bills, but knowing who's creditworthy involves more than a quick glance at a credit report. That's where the five Cs of credit — character, capacity, capital, collateral, and conditions — come into play.

These long-standing principles serve the foundation for sound credit assessments and provide a structured way to assess a customer's creditworthiness, so your team can set credit limits, monitor payments, manage non-payment risks, and take action based on payment behaviors over time.

In this blog post, we'll walk through each of the five Cs in credit management and explain how accounts receivable automation tools can help you tackle repetitive tasks and make faster, more accurate credit decisions without sacrificing accuracy or quality.

First impressions aren't always what they seem, which is why you should use historical data from business credit agencies to determine whether customers have a demonstrated history of good payment behaviors. The main scores to pull are:

Paydex (Dun & Bradstreet): Ranges from 1-100 based on payment history. A score of 80+ indicates payments typically come on or before terms. Below 50 signals consistent late payments.

Intelliscore Plus (Experian): Also 1-100, but factors in company size, industry risk, and public records. Scores above 76 are low risk; below 25 is high risk.

FICO SBSS: Ranges from 0-300, commonly used by SBA lenders. Most lenders set 160-165 as a minimum threshold.

Equifax Business Credit Risk Score: Ranges from 101-992. Higher is better, with scores above 700 considered low risk.

Like consumer credit agencies, business credit agencies monitor how companies borrow money and pay down debts over time. The difference is that business credit agencies provide a more holistic view of a company's financial health by compiling a wide range of publicly available data, including business registration details, sales volume, court judgments, liens, bankruptcies, collections accounts, and credit history inquiries.

Business credit agencies also disclose a key metric that can measure a customer's AR performance: days beyond terms, or the average number of days that bills are paid past a specified due date.

A low DBT signals that a company does a good job of paying bills on time — a less-common negative DBT suggests a company makes payments ahead of time.

Example scenario: a potential customer who has a Paydex score of 72 and a Days Beyond Terms (DBT) of 15 tells you that they typically pay invoices about two weeks late. If your credit policy requires a DBT under 10 for net-60 terms, you might offer net-30 instead—or require a larger deposit upfront.

Before you onboard customers, you want some level of certainty that they can pay for the goods or services that your company is selling.

Analyzing a company's income, existing cash flow, and any debt they're carrying can help you ensure that a potential customer is in good financial health. This is often done by calculating a customer's debt-to-income ratio — or DTI — by comparing their total monthly debt obligations to their gross monthly income. The end result, expressed as a percentage, shows how much of a customer's income should be set aside for debt payments every month.

Generally speaking, a DTI of around 35 percent indicates that a customer is managing their existing debts well and aren't overextending themselves by taking on more than they earn in revenue every month.

Example scenario: If a customer shows monthly revenue of $500K with monthly debt obligations of $150K, that would give them a DTI of 30%—within the healthy threshold. But a $50K order would push their monthly obligations to 40% of revenue. A conservative approach would be to start with a $25K credit limit and review after 90 days of on-time payments.

No one likes to think about worst-case scenarios, but you also want to make sure potential customers have the financial strength to cover the debts accrued by their businesses and are committed to its success.

Simply put, you want to make sure that a customer has the assets and financial resources to cover the cost of any debts that the business may accrue.

In these cases, reviewing the financial statements of key shareholders can help you determine their net worth, as well as find any equity, assets, and investments that can be used as collateral if business debts aren't paid.

Reviewing a company's capital structure can help you determine how much debt and equity is used to finance operations and growth. If a company is relying on borrowed funds more than those offered up by owners and shareholders, it may present some level of risk for your company.

Example scenario: Your review shows the business owner has $2M in personal assets and has invested $500K of their own capital into the company. This "skin in the game" signals commitment—a positive indicator for extending credit. Compare this to a business where the owners have taken out most of their equity; that's a red flag.

When it comes to weighing a potential customer's credit risk, you want to make sure all your bases are covered.

While you're checking financial statements to see what company stakeholders have and determine their net worth, it may be helpful to look at fixed assets — such as real estate, inventory, equipment, and other types of property that can't be converted into cash quickly — especially if a potential customer may be a high credit risk.

Depending on the situation, companies can require high-risk customers to offer fixed assets as collateral when business debts can't be paid.

Example scenario: A customer with a credit score of 58 requests a $100K credit line. You could require a personal guarantee plus a UCC filing on their equipment valued at $60K. If they default, you have a legal claim to those assets.

While much of your credit risk analysis will focus on a potential customer and key stakeholders, it's important to consider other extraneous factors that may impact a company's ability to pay.

Big-picture considerations, such as current market conditions, industry trends, geopolitical tensions, and the broader economic climate, can have significant implications for any business and should be accounted for in your assessment.

There may even be times when these external factors warrant an adjustment to your company's credit policies that specify who should receive it and how unpaid debts should be collected.

Example scenario: An enterprise software vendor tightens terms for customers in sectors facing contraction—moving from net-60 to net-30 and lowering credit limits when a customer's industry shows rising bankruptcy rates. A logistics company does the opposite during e-commerce surges, extending more generous terms to retailers ramping up for peak shipping seasons when payment reliability is historically strong.

Determining whether businesses can pay their bills before they become a customer is the first line of defense against bad debt for your organization.

The problem is that conducting and completing a credit risk assessment can take hours if you're doing much of the research and data entry on your own.

With the help of an AI-powered credit risk management tool, you can automate certain tasks and speed up the customer onboarding process without compromising on the quality of your credit assessments and reviews.

For example, Fazeshift's customer credit agent can automatically log in to credit agencies, pull up a customer's credit history, and enter those details into your enterprise resource planning system, and set credit limits or holds.

Once that's done, another AI agent from Fazeshift can leverage customer onboarding forms to fill out billing details that sync with your ERP, including NetSuite and SAP.

Credit management plays a vital role for businesses and traditional lenders, such as banks, credit unions, and other financial institutions, that want to make sure customers will make good on their promises to pay for goods or services.

Following the five Cs for assessing creditworthiness and incorporating task-oriented AI into your workflow can help you mitigate risks for your organization, minimize potential losses, and ultimately develop solid relationships with customers who pay their bills on time.

Want to find out how Fazeshift's AI agents can automate time-consuming tasks in your credit risk management workflows?

Schedule a demo and see how Fazeshift can give your team more time back by seamlessly carrying out a wide range of accounts receivable tasks—from turning contracts into invoices and managing payment communications with customers.

Eliminate manual bottlenecks, resolve aging invoices faster, and empower your team with AI-driven automation that’s designed for enterprise-scale accounts receivable challenges.